Is USDC Safe?

Introduction

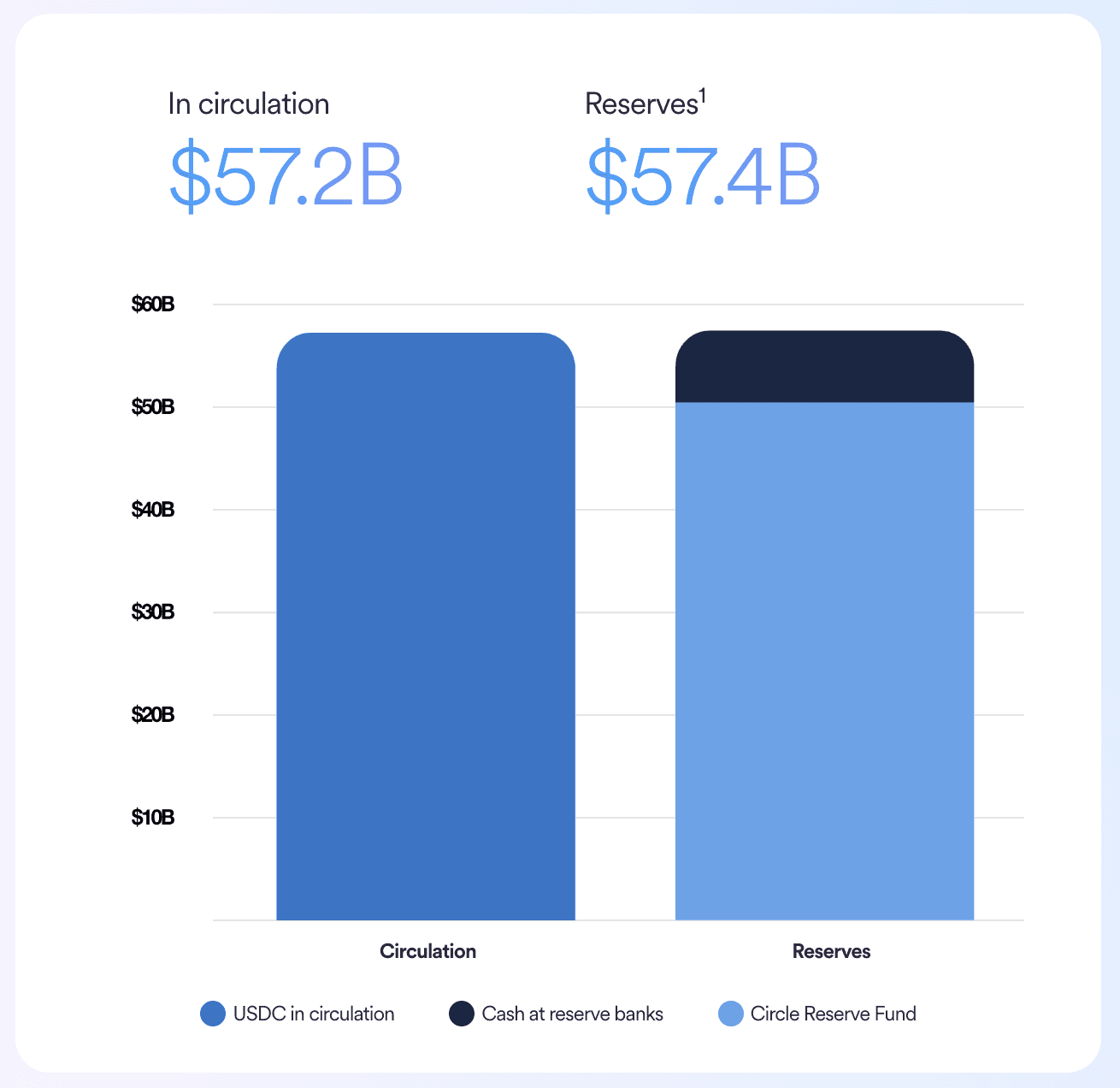

With $57.2B in circulation, USDC is one of the most widely held and used stablecoins. USDC is a cryptocurrency issued by Circle that is designed to represent a US dollar digitally on a blockchain by maintaining a value of $1. This is what makes USDC a “stable” coin; the core goal of the token is to hold a value of $1.

To understand if USDC is safe, we must first understand how USDC is created and where its value comes from. Then we will briefly look at what you can do with USDC and why it has become so widely used across the globe. But before we do all of this, let's first define what “safe” means. In this context, we will define “safe” as meaning:

The value of USDC holds its peg to the dollar (i.e., it stays roughly equal to $1)

Moving between USDC and actual US dollars in a US bank account is seamless

To the extent that both of these are true, we would deem USDC as safe.

The TL;DR is that USDC is largely safe (this is not investment advice of course). Below, we offer a framework to explain how we came to this conclusion.

How is USDC created?

At a high level, to create a US dollar on the internet, Circle, the issuer of USDC, takes a physical dollar and puts it in the bank (it’s slightly more complex, but we will explain below). Then, Circle “mints” a digital dollar on a blockchain (technical details below). This characteristic of backing each digital dollar with a real asset is what makes USDC a full-reserved stablecoin.

Circle allows qualified businesses to open a Circle Mint account. Through this account, businesses deposit the USD that Circle then exchanges for USDC. The reverse happens as well; businesses can deposit USDC into their Circle Mint account and receive US dollars. When Circle exchanges USDC for USD, it “burns” the tokens, taking the USDC out of circulation.

Now let’s dig deeper.

What happens technically?

To create a digital dollar on a blockchain, Circle uses a “smart contract” - code that lives on a blockchain. You can think of smart contracts as mini-software that can be interacted with. When Circle “mints” or “burns” USDC, it is simply executing code in the smart contract. Of all the applications on a blockchain, full-reserved stablecoins are arguably one of the simplest. They are truly a representation of an asset that lives off-chain (not on a blockchain), so their functionality need not be complex.

Now back on the “real-world asset” side where do those US dollars actually sit? As we alluded to above, it’s not quite as simple as $1 sitting in a bank account. In practice, Circle utilizes investments in short-term, low-risk US treasury bills to generate yield and diversify risks from the banking system. As seen in the chart below, 20% of the reserves do actually sit in cash that is spread across 30 of the world’s Systematically Important Banks (SIBs), and the other 80% is in the Circle Reserve Fund.

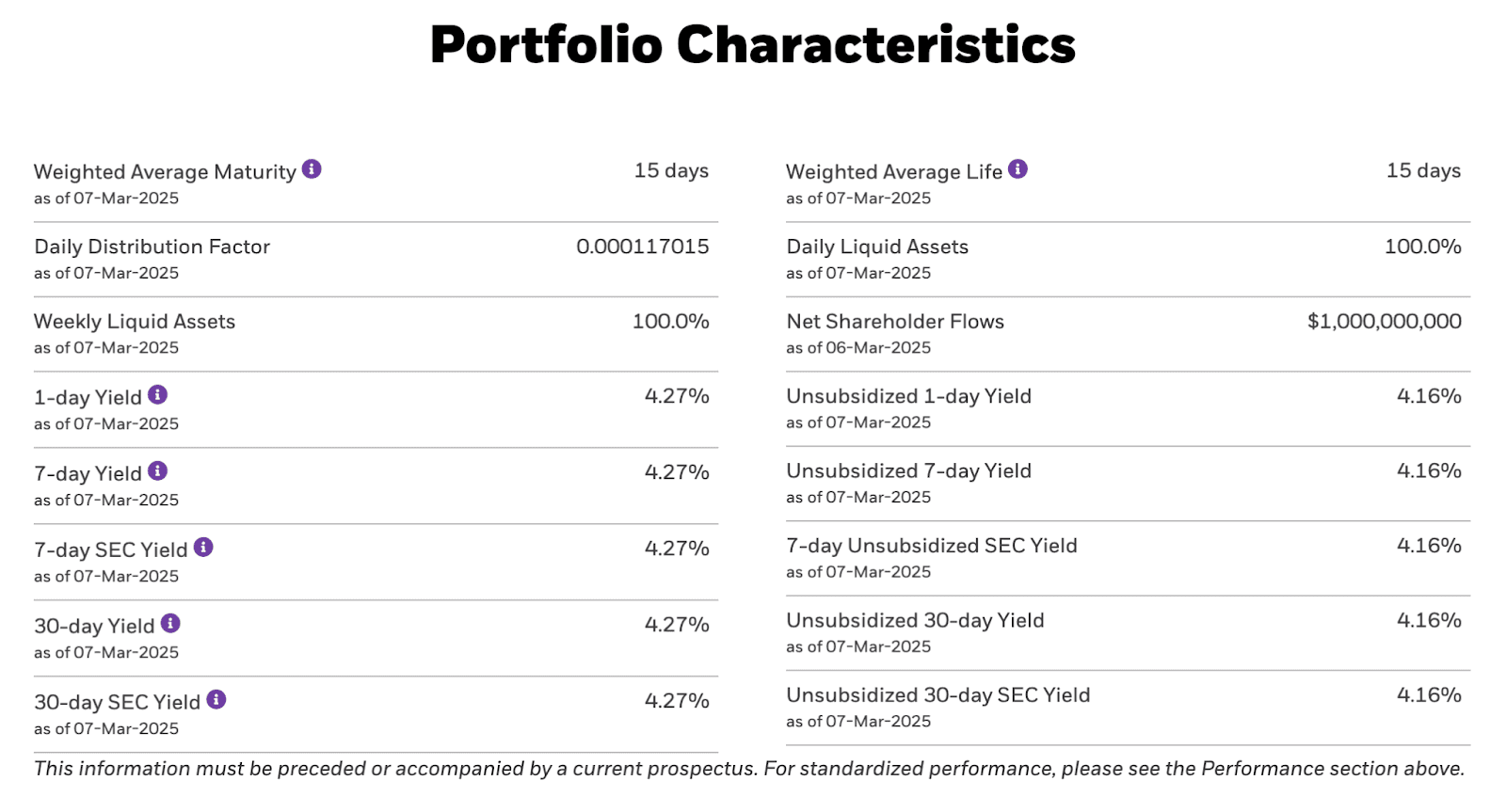

As you can see below, the Circle Reserve Fund is a mix of treasury bills of various short-term durations. In addition to whatever bank interest rate Circle earns on the cash, these treasuries generate yield for Circle enabling it to make interest on the reserves. This provides a further financial cushion for Circle and also makes Circle quite a profitable business in times of high interest rates since it currently does not pass any of these interest earnings on to end holders of USDC. For example, if Circle buys a short-dated US Treasury today for $10,000, in 30 days it would pay out $10,037.50, earning Circle a 4.5% annualized yield.

Is USDC always worth $1?

While minting stablecoins and holding cash and low-risk assets seems just about as safe as it gets, you may be starting to see areas in which there are a few risks (or at least areas that require trust and oversight). What if Circle runs away with my money? What if the smart contract gets hacked? What if Treasury rates decline? Ultimately, it is these risks that influence the price of USDC and determine if the peg holds. To formalize the above questions into a true framework that we can use to assess USDC (and other stablecoins), we can bucket the risks into four types:

1. Liquidity risk: When you knock on Circle’s door and ask for your dollar back, does Circle have cash on hand to give you your dollar back?

2. Counterparty risk: How trustworthy is Circle? Will they run off with your money?

3. Security risks: What if Circle gets hacked and all their money is stolen, or someone starts issuing USDC without it being backed?

4. Legal risks: What if the government deems USDC illegal? Can you still get your money back?

1) Counterparty risk

Counterparty risk assesses the trustworthiness of Circle as an issuer and whether users can rely on the company to honor its obligations. Practically, this means, if you give Circle 1 USDC, will it give you $1 back?

As a regulated financial company based in the United States with significant institutional backing from major financial players, Circle has garnered credibility for its operations. The company has established a track record of maintaining USDC's peg through various market conditions, including during crypto market crashes, demonstrating operational reliability when other stablecoins have faltered.

With that said, it is important to note that USDC did experience a brief period where its peg to the USDC dollar was broken during the March 2023 US banking crisis where Silicon Valley Bank, Signature Bank, and First Republic Bank experienced runs on their reserves. Like many startups, Circle had a portion of its cash sitting at Silicon Valley Bank (SVB). At the time, Circle had $3.3B of its $40B in reserves at SVB, which caused investor concerns about Circle’s ability to access that cash. This caused the peg to break, and USDC briefly declined to $0.88 before returning to the peg within a few days. To Circle’s credit, they quickly stepped in to clarify that they had sufficient additional reserves to cover the shortfall even if the $3.3B were to be lost. Fortunately, that scenario never played out.

Following this brief period of market turbulence, Circle has taken additional steps to further diversify its assets across 30 global banks and reduce its exposure to any one bank to avoid the repeat of a scenario like the one above. Circle also has long-term ambitions of parking its funds directly with the US Federal Reserve although this plan is currently dependent on the passage of stablecoin legislation in the US.

Throughout its history, Circle has proactively worked with regulators and obtained relevant licenses in multiple jurisdictions, positioning USDC as a compliant stablecoin in an increasingly regulated environment. Independent accounting firms regularly verify that USDC is fully backed by appropriate reserves through attestations, which reduces the risk of fractional reserve practices that have affected other stablecoins.

Circle's corporate governance structure, with established leadership and institutional oversight, provides additional assurance that the company operates with long-term stability in mind rather than short-term profit maximization that could jeopardize reserves.

2) Liquidity risk

The ability to easily move in and out of an asset is described as its liquidity. Assets that are easy to buy or sell have high liquidity, while assets that are hard to buy or sell have low liquidity. For example, Apple’s stock is highly liquid as you can easily buy or sell it on an exchange. Conversely, the market for an antique lamp might be very small, making it difficult to sell and thus not very liquid.

In this case, the liquidity of USDC is concerned with how easily you can convert your USDC back to USD at the expected $1 value. Since Circle does not keep every dollar sitting in cash in the bank, but rather buys dollar-like assets, such as short-dated US Treasuries, and overnight US Treasury repurchase agreements, you must look at how liquid these assets are. In general, these assets are considered highly liquid and safe, providing a strong foundation for maintaining USDC's value. However, during periods of market stress, even Treasuries can experience price fluctuations. If Circle needs to sell treasury holdings before maturity during rising interest rates, they might realize losses, potentially affecting their ability to maintain the peg in extreme circumstances.

One other thing to note about liquidity is the wide availability of USDC across global exchanges.USDC has significant secondary market liquidity across major cryptocurrency exchanges and DeFi platforms like Coinbase, Uniswap, and Binance. These avenues allow holders to exchange USDC for USD at market rates and swap from USDC to other assets. Because USDC is being swapped outside of Circle, the price of the swap may not be exactly $1 as market makers take a fee for this service and price in the risks outlined here.

3) Security risk

Security risk involves the technical infrastructure underlying USDC and the protections in place to prevent exploitation. On EVM chains like Ethereum, Polygon, and Base, USDC uses standard ERC-20 contracts, which have been extensively audited and battle-tested in the market. These standardized implementations reduce the likelihood of vulnerabilities compared to more experimental smart contract designs. Circle maintains centralized control over the minting and burning functions, which provides protection against unauthorized issuance but creates a central point of failure that differs from more decentralized cryptocurrencies.

USDC operates across multiple blockchains, which diversifies technical risk by not being dependent on a single network's security but also increases the attack surface and complexity of maintaining secure operations across different platforms. Circle employs industry-standard security practices for key management and operational procedures, with multiple layers of protection for critical systems, though specific details are not publicly disclosed for security reasons. The company has demonstrated resilience against hacks targeting its infrastructure thus far, though the growing value of assets under management increases the incentive for potential attackers.

4) Legal risks

The regulatory environment for stablecoins continues to evolve globally, creating both opportunities and challenges for USDC. In the United States and other major jurisdictions, there is increasing regulatory clarity around stablecoins, with Circle positioning USDC as a compliant option that meets emerging standards. This proactive approach may provide USDC with advantages as regulations formalize, while more resistant competitors may face challenges.

Circle has established relationships with regulated financial institutions, providing reliable pathways for fiat on/off-ramps that are likely to remain available even as regulatory scrutiny increases. Different jurisdictions have varied approaches to stablecoin regulation, which could impact USDC's global availability, but Circle's focus on compliance may help navigate this complex landscape. If regulatory actions were taken against USDC, Circle has indicated they maintain procedures to ensure users could redeem their holdings, though the process might experience delays during a transition period.

USDC use cases

As we have explored in the previous section, USDC does have some risks, but in our overall assessment, it is a relatively safe digital asset. Its track record of strong governance and global liquidity has made it a preferred token for commerce and all types of payment use cases. These use cases include international remittances, merchant payments, bill pay, and salary payments. In the decentralized finance (DeFi) space, USDC plays a crucial role in various applications such as lending, borrowing, and yield farming. Its stability makes it an attractive option for use as collateral in smart contracts without fear of major price swings.

As we look into the future, we see USDC having an increasingly important role in global commerce. Businesses and individuals can use USDC payments for efficient global transactions, leveraging its ability to settle transactions in seconds worldwide, at any time, and for near-zero cost.

At Loop Crypto, we see this ourselves. We offer a crypto payment API, a checkout solution for recurring crypto payments, and crypto invoicing tools. Roughly 90% of all the payments our merchants receive are in USDC, showcasing how it is a preferred payment method. Accepting USDC opens up the opportunity to reach 500 stablecoin holders that span across 155 countries. It’s a massive market opportunity for businesses.

For our merchants, some of the most important benefits are its stability and liquidity. When they are paid 1 USDC, they know that token will hold its value as 1 US dollar. There are no concerns about wild price swings. USDC’s liquidity is also crucial as merchants may need to be able to quickly off-ramp to pay expenses in fiat. Another key point is USDC’s global interoperability. As a blockchain-based token, USDC is available across the globe. This makes accepting payments from international customers significantly easier and lower cost.

On the consumer side, paying with USDC also makes sense. USDC’s stability is again appealing as consumers typically do not want to pay in tokens like Bitcoin and ETH that are likely to appreciate in value over time. Paying in USDC also puts consumers in control. They do not have to trust a merchant with their credit card details, and they can easily confirm all their payments on chain.

Conclusion

USDC demonstrates strong safety characteristics relative to other digital assets in the cryptocurrency ecosystem. It maintains full reserves verified through regular attestations, creating transparency that builds user confidence. However, no asset is without risk, and potential USDC users should be aware of certain considerations. In extreme market conditions, maintaining the exact $1 peg might be temporarily challenged, as witnessed during past market disruptions when USDC briefly traded below its target value.

The centralized control model wherein the Circle Foundation controls the smart contract provides security benefits, but it does create dependencies on Circle's operations and decision-making. This may not appeal to users seeking truly decentralized solutions.

For most users seeking digital dollars for everyday transactions, payments, or as a temporary store of value in the digital asset ecosystem, USDC provides a relatively safe option compared to more volatile cryptocurrencies when you look at other altcoin payments. USDC’s widespread adoption across centralized and decentralized finance platforms, high liquidity in secondary markets, and transparent reserves make it one of the more reliable stablecoins in the market. USDC has weathered significant market turmoil, including the collapse of other stablecoins and major crypto institutions, which speaks to its resilience under stress conditions.

Remember that this analysis is not investment advice, and users should conduct their own research and risk assessment based on their specific needs and risk tolerance. As with any financial instrument, diversification remains an important principle, and users should consider their overall exposure to any single asset or platform within their broader financial strategy.

FAQ

What blockchains have USDC?

USDC is natively supported for 18 blockchain networks: Algorand, Aptos, Arbitrum, Avalanche, Base, Celo, Ethereum, Hedera, NEAR, Noble, OP Mainnet, Polkadot, Polygon PoS, Solana, Stellar, Sui, Unichain, and ZKsync – with more expected in the future. USDC has also been bridged to many emerging blockchains by third-party bridges, resulting in the creation of bridged forms of USDC such as USDC.e.

What is wrapped USDC vs Canonical USDC?

The difference between wrapped USDC (often referred to as "bridged USDC") and canonical USDC lies in their issuance, use cases, and how they are backed.

Canonical USDC is the native form of USDC issued directly by Circle on a specific blockchain. It is fully backed by reserves held by Circle and is redeemable 1:1 for U.S. dollars. Canonical USDC is considered the "official" version of USDC on a blockchain and is interoperable across multiple supported networks via Circle's Cross-Chain Transfer Protocol (CCTP). This makes it highly trusted and widely used in applications where stability and direct redemption are critical, such as payments, DeFi lending, and trading.

Wrapped or Bridged USDC, on the other hand, is a version of USDC created when native USDC from one blockchain is locked in a smart contract, and an equivalent amount of bridged USDC is issued on another blockchain. Bridged USDC is not issued or directly redeemable by Circle but serves as a proxy to bootstrap liquidity on new or less-established blockchains. While it helps jumpstart activity in ecosystems, it can lead to liquidity fragmentation since it depends on third-party bridge providers. However, Circle has introduced the Bridged USDC Standard to allow seamless upgrades from bridged to canonical USDC when Circle takes over ownership of the bridged token contract.

Is USDC a cryptocurrency?

USDC is a fully reserved stablecoin, which is a type of cryptocurrency, or digital dollar. Unlike other cryptocurrencies that fluctuate in price, USDC is designed to maintain price equivalence to the US dollar. USDC is a stable store of value that benefits from the speed and security of blockchain technology.

How can you get USDC?

Directly from the issuer

Circle allows qualified businesses to open a Circle Mint account. When a business deposits USD into its Circle Account, Circle issues the equivalent amount of USDC to the business. The process of issuing new USDC is known as “minting.” This process creates new USDC in circulation.

Similarly, when a business wants to exchange its USDC for US dollars, the business can deposit USDC into its Circle Mint account and request to receive US dollars. This process of redeeming USDC is known as “burning.” This process takes USDC out of circulation.

From an exchange

When US dollars are swapped for USDC on a digital asset exchange, the exchange will typically provide the balance of USDC it has on-hand to fulfill the swap. If the exchange needs more USDC to fulfill the swap, the exchange will often use its Circle Mint account to mint more USDC.

Finally, you can of course be paid in USDC if you have a crypto wallet. Loop Crypto is a leading USDC payment gateway enabling payment processors and merchants to integrate USDC payments.