A guide to stablecoin payments

What is a stablecoin?

In this article, we offer a guide to understanding stablecoins and how they are being used for payments. Before we dig into the payments use case, though, we need to start with the basics: what is a stablecoin?

Stablecoins are a tokenized representation of an on or off-chain asset (or assets) that are designed to maintain a consistent value. As of this writing in early 2025, the most widely circulated stablecoins are fiat-backed stablecoins. These stablecoins are typically tied to the value of the US dollar. USDC and USDT are popular examples of fiat-backed stablecoins where the token is a representation of a physical dollar that sits in a bank account and can be redeemed one-to-one.

Fiat-backed stablecoins are not the only game in town though. As we will investigate further throughout this article, there are many different flavors of stablecoins that are each purpose-built for distinct use cases. For example, there are also stablecoins backed by digital assets (e.g., see the DAI stablecoin). There is also a broad range of algorithmic stablecoins that are not necessarily backed by collateral but instead utilize a minting and burning mechanism tied to an underlying function.

In the next section, we will dig a bit deeper into classifying stablecoins and provide a framework for bucketing all the different types of stablecoins in the world.

What are the different types of stablecoins?

Stablecoins can generally be bucketed into two groups: asset-backed and algorithmic, sometimes referred to as synthetic stablecoins. Although this graphic is now a bit dated, this original taxonomy of stablecoins from JPMorgan Chase published in February 2020 has largely withstood the test of time and gives a nice visual of the different buckets of stablecoins. Of course, Libra, the failed Facebook stablecoin, is no longer around, and “MAKER” is now known just as DAI.

Asset-backed stablecoins

With asset-backed stablecoins, the issuer takes a physical dollar and puts it in a bank (there’s slightly more nuance to this, but that’s the general gist). Then the issuer “mints” a digital dollar on a blockchain. The reverse happens as well; businesses can deposit the stablecoin with the issuer, who then “burns” the tokens, taking them out of circulation. Some of the most popular dollar-backed stablecoins are USDC, USDT, and PYUSD.

To really understand how asset-backed stablecoins work, let’s take Circle (the creator of USDC) as an example. To create a digital dollar on a blockchain, Circle uses a “smart contract”-- code that lives on a blockchain. You can think of smart contracts as mini-software that can be interacted with. When Circle “mints” or “burns” USDC, it is simply executing code in the smart contract. Of all the applications on a blockchain, full-reserved stablecoins are arguably one of the simplest. They are truly a representation of an asset that lives off-chain (not on a blockchain), so their functionality need not be complex.

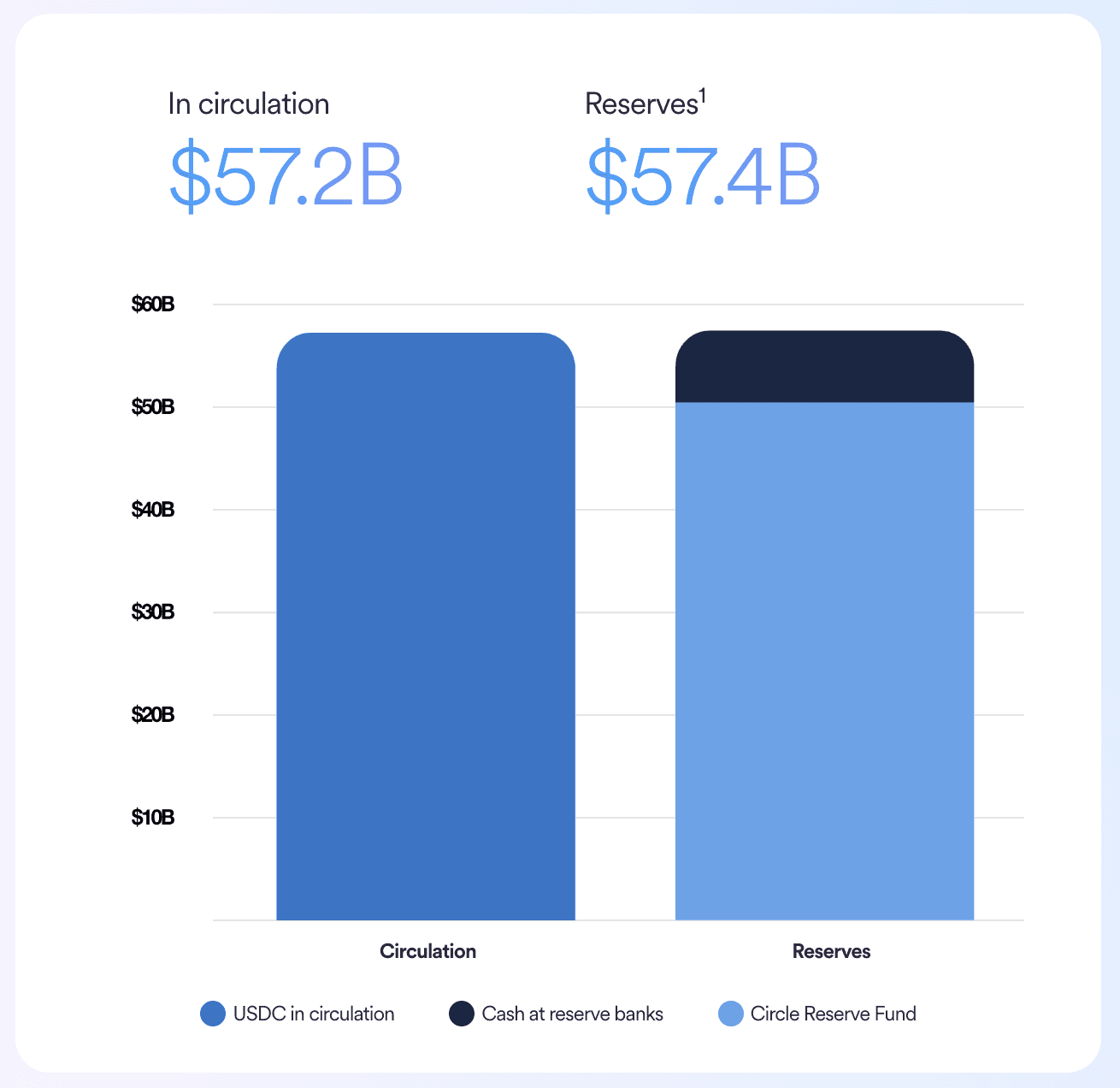

Now back on the “real-world asset” side, where do those US dollars actually sit? As we alluded to above, it’s not quite as simple as $1 sitting in a bank account. In practice, Circle utilizes investments in short-term, low-risk U.S. Treasury bills to generate yield and diversify risks from the banking system. As seen in the chart below, 20% of the reserves do actually sit in cash that is spread across 30 banks, including some of the world’s Systematically Important Banks (SIBs), and the other 80% is in the Circle Reserve Fund.

While USDC and USDT are technically “fiat-backed” stablecoins, a subcategory within asset-backed stablecoins, the backing of a stablecoin does not have to be fiat. DAI is a good example. While DAI’s peg to the US dollar is partially based on holding dollars via USDC, it also holds Bitcoin, Ether, and other cryptocurrencies to maintain the value of the token. More on-chain stablecoins, like DAI, can often be overcollateralized, backing every digital dollar with, say, $2 worth of assets, which allows for some price movements.

Algorithmic stablecoins

An algorithmic stablecoin is a type of cryptocurrency designed to maintain a stable value—usually pegged to a fiat currency like the US dollar—through the use of algorithms and smart contracts, rather than being backed by actual reserves of cash or crypto assets. That last point is really critical. Unlike the asset-backed stablecoins we talked about above, there is no physical dollar in the bank or Bitcoin locked up in a smart contract that can be redeemed. While USDC or USDT hold equivalent reserves in bank accounts or other assets, algorithmic stablecoins rely on supply-and-demand mechanics. The underlying protocol automatically expands or contracts the coin’s supply based on market conditions to keep its price near the target value.

To achieve this, the system might mint new coins when the price rises above the peg (to increase supply and drive the price down) or burn coins when the price falls below the peg (to reduce supply and drive the price up). Some designs also involve a second token to absorb volatility—this "companion" token might take on risk and reward in exchange for helping stabilize the main stablecoin. While the idea is innovative and fully decentralized in theory, these systems can be fragile and vulnerable to sudden shifts in market confidence, as seen in high-profile failures like TerraUSD (UST).

Are stablecoins actually stable?

The most popular and trusted stablecoins like USDC and USDT have a long history of being stable. In practice, you might not see these coins trading exactly at 1:1 with their pegged assets, but this is due to market supply and demand dynamics, liquidity differences across exchanges, and perceived risk factors about the stablecoin issuer. These forces create small but persistent price deviations, which are typically minimal (within ±0.5%). This deviation can widen though during market stress or when confidence in the issuer declines. Check out our other blog article titled “Is USDC Safe” for further discussion on this topic.

The history of algorithmic or synthetic stablecoins is a little more colored. TerraUSD, the Terra blockchain’s stablecoin, depegged in May 2022 and went to $0. If you want to learn more about the Terra Luna saga, there is a ton of analysis out there. You can start with this article. We will see how algorithmic stablecoins continue to evolve, but to date, asset-backed stablecoins, particularly those backed by fiat assets, have proven to be much more resilient.

Why are stablecoins used for payments?

We’ve been spending a lot of time explaining what stablecoins are and how they work, but let’s turn now to payments. Why are stablecoins used for payments? There are a number of reasons stablecoins are ideal means of payment and are increasingly becoming a dominant form of payment around the world. In the sections below, we dive into some of the key reasons.

(1) Global Interoperability

Stablecoins are inherently digital and borderless, which makes them globally interoperable. This means they can be used by anyone with an internet connection, regardless of where they are in the world. Unlike traditional fiat currencies, which are geographically bound—e.g., you can't easily spend British pounds in the U.S. or Japanese yen in Brazil—stablecoins like USDC, USDT, or DAI can be sent, received, and accepted anywhere in the world with compatible wallets or infrastructure. For example, a freelance graphic designer in Argentina can be paid instantly in USDC by a client in Germany without worrying about currency conversion or banking restrictions. This global flexibility is especially valuable in emerging markets where access to traditional banking services may be limited.

(2) Instant Settlement

Stablecoin payments settle almost instantly on the blockchain. When a transaction is made, the recipient sees the funds in their wallet within seconds or minutes, depending on the network. There's no need to wait for “cleared” funds like with bank transfers or card payments, which can take 1–3 business days (or longer for cross-border transactions). For example, sending USDC on the Solana network is near-instant and costs fractions of a cent, whereas receiving a wire transfer might take days and cost $30 or more in fees. Instant settlement can be a game-changer for merchants and individuals, improving cash flow and eliminating payment uncertainty.

(3) Lower Costs

Stablecoin transactions can be significantly cheaper than traditional payment methods. Credit card processors typically charge merchants 2.5%–3.5% per transaction, plus potential fixed fees. For example, if a customer pays $100 via Visa or Mastercard, the merchant might only receive $96.50 after processing fees. In contrast, sending stablecoins like USDC on networks like Solana or Tron can cost as little as $0.001–$0.01 per transaction. Even Ethereum, which is more expensive, can cost just a few cents to a couple of dollars depending on network congestion, still often cheaper than credit card fees for high-value transactions. This cost reduction can meaningfully impact profit margins, especially for businesses operating at scale.

(4) Yield Opportunities

Some stablecoins offer the ability to earn yield simply by holding them, especially when stored in decentralized finance (DeFi) platforms or yield-bearing accounts. For example:

DAI held in the Dai Savings Rate (DSR) through MakerDAO can earn yield directly from the protocol.

USDC can be deposited into platforms like Aave or Compound, where holders can earn interest from borrowers.

Centralized platforms like Coinbase or Crypto.com also offer interest on USDC holdings, sometimes ranging from 2% to 6% annually depending on the terms.

For merchants or individuals who prefer to keep funds on hand, the ability to earn passive yield on stablecoins adds another layer of utility, effectively turning working capital into an income-generating asset.

(5) Price Stability Compared to Crypto

Traditional cryptocurrencies like Ethereum (ETH) or Bitcoin (BTC) are highly volatile, which makes them less ideal for routine payments. For example, if you accept a $100 payment in ETH, its value could swing to $90 or $110 within a day due to market fluctuations. Stablecoins solve this problem by being pegged to a stable asset, typically the U.S. dollar. This makes stablecoins like USDC, USDT, and BUSD a safer option for both payers and recipients, preserving value and predictability. It's much easier for a merchant to price goods and accept payments in a currency that doesn’t fluctuate dramatically.

How do I start accepting stablecoins for payment?

Now that we’ve laid out all of the value propositions around accepting stablecoins, let’s talk about how you get started if you’re a merchant looking to accept payment in stablecoins. Here are the 5 high-level steps you need to follow.

(1) Set up a wallet

First, you’ll need a crypto wallet that can receive and hold stablecoins. You have two main options:

Custodial wallets (e.g., Coinbase Commerce, Binance Pay, or BitPay): These are easy to use and great for beginners because you do not have to worry about trying to store or remember a private key. With a custodial wallet, you are trusting someone else (i.e., a custodian) to keep your funds secure. While some individuals and companies may be philosophically opposed to this model, custodians are experts in security and have world-class technology in place to keep funds safe.

Non-custodial wallets (e.g., MetaMask, Phantom, or hardware wallets like Ledger): You hold the keys, which means you have full control of your funds, but also full responsibility. This option is better for those who want more independence or are comfortable managing wallets themselves. If you want a non-custodial option with more security, you can consider a multi-signature wallet, like a SAFE. Particularly for businesses where there a multiple owners, a SAFE provides extra security because it requires multiple parties to sign off on any fund movement.

As you select a wallet, you should note that some are tailored for specific chains. The big wallet providers generally support the most widely used chains, but make sure that the wallet you select can support popular stablecoins (e.g., USDC, USDT, DAI) and the networks you plan to use (Ethereum, Solana, Polygon, etc.).

(2) Decide which stablecoins and networks to use

We have talked about stablecoins being globally interoperable. While that is technically true, there are some considerations when it comes to geographic regions and the chains and tokens used. For example, USDT on TRON is known as being very popular in Asian markets. If you are in North America though, most users may be less familiar with TRON and instead hold USDC on Ethereum and Solana. The chart below shows how dominant BNB Smart Chain and TRON are when it comes to USDT volumes.

As you think about the correct mix of stablecoins and blockchains to receive payment in, make sure you are considering your local market dynamics. Here are a few tips and trends for you.

USDC on Solana or Polygon – fast, cheap, and widely accepted

USDT on Tron – low fees and very popular in some regions

DAI on Ethereum or Arbitrum – decentralized and DeFi-native

You’ll want to consider your customers’ preferences too. If you’re targeting users in crypto-savvy regions, ask which stablecoins they already use.

(3) Integrate with your website or storefront

As we’ll explore later, this is where Loop Crypto comes in. We make it simple to embed a crypto payment checkout experience within your signup process. Depending on the type of business you are running, you may have a variety of payment use cases. We offer a crypto payment API, a checkout solution for recurring crypto payments, and crypto invoicing tools. Over 90% of all the payments our merchants receive are in stablecoins, showcasing how it is a preferred payment method. Accepting stablecoins opens up the opportunity to reach 500M stablecoin holders that span across 155 countries. It’s a massive market opportunity for businesses. A crypto payment processing solution like Loop will be able to accommodate all of these different payment methods on a variety of blockchains.

(4) Figure Out What to Do with the Funds

Once you've set up your crypto payment processor and begin receiving payments in stablecoins, the next step is managing those funds effectively. In many cases, you’ll want to convert your stablecoins into fiat currency right away, especially if your business operates primarily in dollars, euros, or another national currency. This ensures you have cash on hand for recurring expenses like rent, payroll, taxes, or inventory. For example, you might receive $5,000 in USDC and immediately convert it through Coinbase or Binance to cover your monthly software subscriptions and team salaries. However, if your business operates more natively in the crypto ecosystem—such as a DAO, NFT project, or Web3 service—you may not need to exit to fiat at all. Instead, you can use stablecoins directly to pay on-chain contributors, freelancers, or even vendors who accept crypto payments, saving time and reducing conversion costs.

Once your immediate expenses are covered, you can put your idle stablecoin balances to work. There are a variety of yield-bearing opportunities available both on-chain and through custodial platforms. Some stablecoins like DAI offer native yield through protocols like MakerDAO, while others—such as FRAX or sDAI (a yield-bearing wrapper for DAI)—are designed specifically to grow in value over time. Although commonly used stablecoins like USDC and USDT don't automatically generate yield, they can be deposited into decentralized finance (DeFi) platforms like Aave, Compound, or Yearn to earn interest. Additionally, centralized services such as Coinbase and Circle offer yield-bearing accounts for USDC, providing a more traditional user experience. If you’re willing to swap your USDC for something like USDY or aUSDC (Aave’s interest-accruing version of USDC), you can retain the benefits of price stability while earning passive income on your business treasury.

(5) Consider any accounting implications

Depending on where you're based and how much you're transacting, you may need to track stablecoin income for taxes or reporting. Most crypto accounting tools (like CoinTracker or Koinly) support stablecoins and can help you stay organized. We have another post on crypto accounting infrastructure that will walk you through the implications of accepting stablecoins as payment. In short, accepting stablecoins (rather than volatile crypto assets) tends to generally simplify accounting since you can track a stablecoin's value at 1:1 with the US dollar.

Conclusion

In this article, we started by establishing a basic definition and taxonomy of what a stablecoin is. From there, we went on to explore different stablecoin examples to understand how these tokens maintain their consistent value. This consistent value makes them an ideal digital asset to use for payments. As we dug into, there are a variety of benefits for merchants when it comes to accepting stablecoins as a payment method. These include global interoperability, low fees, and instant settlement. With the recent emergence of yield-bearing stablecoins, there are increasing opportunities to earn funds just for holding stablecoins as well. Finally, we outlined five high-level steps that merchants can take to get started today in accepting stablecoins.

Loop Crypto is designed to make it simple to accept stablecoins. If you’re ready to seize the stablecoin opportunity by enabling the world’s fastest-growing payment method, let’s talk!

FAQs

Are stablecoins always worth $1?

In practice, Stablecoins don't trade exactly at 1:1 with their pegged assets due to market supply and demand dynamics, liquidity differences across exchanges, and perceived risk factors about the stablecoin issuer. These forces create small but persistent price deviations, which are typically minimal (within ±0.5%) for well-established stablecoins but can widen during market stress or when confidence in the issuer declines.

How are stablecoins different from other tokens?

The biggest difference between stablecoins and other tokens is their price stability. Stablecoins are specifically designed to maintain a fixed value—usually pegged to a fiat currency like the U.S. dollar. For example, 1 USDC ≈ $1. This makes them ideal for payments, savings, and as a hedge against crypto volatility.

Other tokens (like ETH, SOL, or UNI) fluctuate in value based on market demand. They're more like investments or utility tokens within a network—used for staking, governance, paying gas fees, or speculation. For example, the price of ETH could swing by 5–10% in a single day, making it risky for everyday transactions or storing value.

Does the network a stablecoin is on matter?

If you are a merchant accepting stablecoins, you will want to consider which networks you make available. In certain geographies, some stablecoins are more popular than others. For example, USDT on TRON is very popular in emerging markets. When it comes to networks, there can also be different few dynamics for sending funds. For example, transactions on Ethereum tend to be more expensive then using layer-2 solutions like Celo or Base.

How can merchants start accepting stablecoin payments today?

Loop Crypto makes it simple for merchants to accept stablecoin payments. We offer a crypto payment API, a checkout solution for recurring crypto payments, and crypto invoicing tools. Over 90% of all the payments our merchants receive are in stablecoins, showcasing how it is a preferred payment method. Accepting stablecoins opens up the opportunity to reach 500M stablecoin holders that span across 155 countries. It’s a massive market opportunity for businesses.